The new home market was stuck in neutral through midyear

The June housing market was nothing to write home about, with sales declining by 4.2% month-over-month. Sales remained up 1.8% year-over-year, but the annual increase was largely driven by more communities being open and builders leaning more heavily on incentives and discounts. Meanwhile, quick move-in supply remained reasonably healthy as builders continue to take a cautious approach to spec home construction amid cooler demand conditions.

Against this backdrop, many builders have been forced to accept that they have limited influence over the broader forces shaping today’s housing market. Higher-for-longer mortgage rates, economic uncertainty, labor market concerns, and the rising cost of living are largely outside their control. What builders can influence, however, is the fear holding consumers back. Many of today’s prospective buyers worry about purchasing at the wrong time, overpaying for a home, or making a decision that ultimately feels like a mistake.

The industry’s opportunity, then, is to replace fear with confidence by giving consumers a compelling reason to move through homes and communities that offer both desirability and long-term value.

“While the market is slow and every sale may feel harder to earn, the industry will still collectively sell between 4 million and 5 million homes across the new and resale markets in 2026,” said Ali Wolf, chief economist for Zonda and NewHomeSource. “Success comes down to identifying the households that still want or need to move and helping them get to a point where they are not just comfortable buying a home, but excited about it.”

New home sales supported by widespread incentives

Zonda’s new home sales metric counts the number of new home contract sales each month and accounts for both cancellations and seasonality. This metric shows there were 700,468 new homes sold in June on a seasonally adjusted annualized rate. This was a decline of 4.2% from last month but an increase of 1.8% from a year ago. On a non-seasonally adjusted basis, 58,678 homes were sold, 2.3% higher than last year and 4.9% above the same month in 2019.

While these sales figures look healthy, incentives are still common in today’s housing market. In June, 63% of new home communities offered incentives on to-be-built homes and 80% on quick move-in supply. Note, these are only publicly available incentives so will underrepresent overall usage.

PSI up YOY but down MOM

Zonda’s New Home Pending Sales Index (PSI) was created to help account for fluctuations in supply by combining both total sales volume with the average sales rate per month per community. The June PSI came in at 133.0, representing a 2.6% rise from the same month last year. The index is currently 23.7% below cycle highs. On a month-over-month basis, seasonally adjusted new home sales decreased 1.5%.

- The markets that posted the best numbers relative to last year were Salt Lake City (+27.5%), Washington, DC (+27.3%), and New York (+26.3%). Salt Lake City was up compared to last year and was flat month-over-month.

- Inversely, the metros that performed the worst year-over-year were Minneapolis (-15.1%), Atlanta (-8.7%), and Raleigh (-7.4%).

- On a monthly basis, Minneapolis, Denver, and Las Vegas were the best performing markets. Minneapolis increased 8.6% relative to last month.

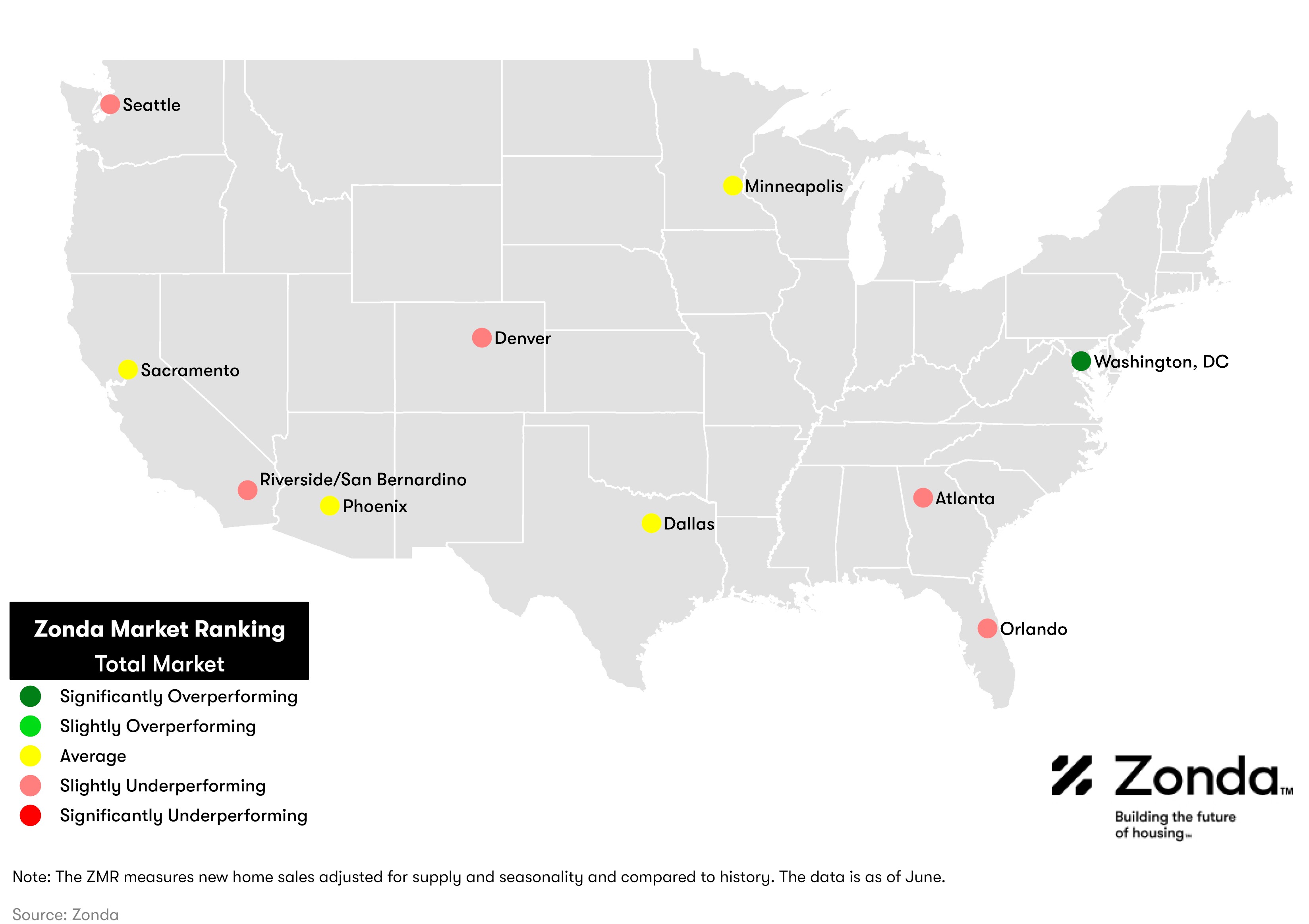

Over half of major markets were average

In order to add further context to sales, Zonda created the Zonda Market Ranking (ZMR). The ZMR accounts for both sales pace and volume, is seasonally adjusted, and is taken as a percentage relative to a baseline market average. Based on the percentage above or below baseline, markets are bucketed into performance groups ranging from significantly underperforming to significantly overperforming relative to historical activity.

The map below shows a snapshot of top production markets by region. Zonda also offers the ZMR for entry-level, move-up/move-down, and high-end markets. Subscribers of the National Outlook report can access all top markets and the tiered breakdown in Zonda’s portal. Non-subscribers can access the tiered maps for the select 10 markets by clicking below.

- The National ZMR index came in at 95.6 in June, which continued to indicate an average market.

- Zonda’s snapshot markets were split between 10% overperforming, 40% average, and 50% underperforming. Among Zonda’s top 55 major markets, 14% were overperforming, 53% were average, and 33% were underperforming.

- Importantly, the ZMR does not account for what it takes to sell a home. For example, securing a sale might still feel difficult in a significantly overperforming market, but if the incentives offered result in a sale, we count the sale.

Pricing gains uneven across tiers

National home prices increased 1.1% year-over-year for move-up homes to $513,669 and 5.3% in the high-end market to $945,765. Prices fell 0.6% for entry-level to $315,676. The rise among higher priced homes reflects new communities opening at higher price points, improvements in design quality, larger lots and home sizes, and/or better locations.

Supplementing our data with a survey Zonda conducts monthly, 21% of builders lowered prices in June month-over-month, 63% held prices flat, and 16% raised prices. In May, for comparison, 21% of builders lowered prices, 66% held prices flat, and 13% increased prices.

Community counts show modest growth

There are currently 17,751 actively selling communities tracked by Zonda, up 3.8% from last year. On a month-over-month basis, the national figure grew 0.3%. Total community count is 8.3% below the same month in 2019. Zonda defines a community as anywhere five or more units are for sale.

- San Jose (+50.0%), Miami (+32.4%), and Greenville (+24.2%) grew community count the most year-over-year.

- Relative to last year, the biggest community count declines were in Minneapolis (-8.9%), Albuquerque (-8.8%), and Fort Collins (-8.5%).

Over the past 18 months, builders have taken a more measured approach to spec home construction to avoid adding excess inventory amid softer demand. As a result, national quick move-ins (QMIs) totaled 35,431, down 9.1% compared to last year and 1.5% lower month-over-month. Total QMIs are 70.8% above 2019 levels. QMIs are homes that can likely be occupied within 90 days.

- On a metro basis, 40% of Zonda’s select markets increased QMI count year-over-year.

- The markets that grew the most year-over-year were San Francisco (+100.0%), Cincinnati (+56.0%), and Philadelphia (+23.8%).

- Cincinnati, Las Vegas, and Sacramento have seen the most growth in QMIs compared to the same time in 2019, up 327.8%, 233.7%, and 208.3%, respectively.

QMIs per community is a good way to track how new home supply looks in the context of actively selling projects. There were 2.1 QMIs per community nationally in June, in-line with the same month last year.

Please note, the QMI per community data aligns with this report covering June trends. Our quick move-in data is weekly, and we release the latest available at the time of publishing this report. As such, recreating the visual below with the data above will yield slightly different results.

Are you interested in seeing past National Housing Market Update and Pending Sales Index reports? Access our report library to learn more.

Methodology

The Zonda New Home Pending Sales Index (PSI) is built on proprietary, industry-leading data that covers 85% of the production new home market across the United States. Reported number of new home pending contracts are gathered and analyzed each month. Released mid-month, the New Home PSI is a leading indicator of housing demand compared to closings because it is based on the number of signed contracts at a new home community. Zonda monitors 17,000 active communities in the country and the homes tracked can be in any stage of construction.

The new home market represents roughly 10% of all transactions, allowing little movements in supply to cause outsized swings in market activity. As a result, the New Home PSI blends the cumulative sales of activity recently sold-out projects with the average sales rate per community, which adjusts for fluctuations in supply. Furthermore, the New Home PSI is seasonally adjusted based on each market’s specific seasonality and removes outliers to reduce volatility. The index was re-benchmarked in June 2026, so PSI readings may differ from those reported in prior releases.

About Zonda

Zonda provides data-driven housing market solutions to the homebuilding industry. From builders to building product manufacturers, mortgage clients, and multifamily executives, we work hand-in-hand with our customers to streamline access to housing data to empower smarter decisions. As a leading brand in residential construction, our mission is to advance the home building industry, because we believe better homes mean better lives and stronger communities. Together, we are building the future of housing.