Zonda’s New Home Lot Supply Index (LSI) for 4Q25, rose for the sixth consecutive quarter and again showed lot supply loosened both year-over-year and quarter-over-quarter across the United States. The index is a residential real estate indicator based on the number of single-family vacant developed lots (VDL) and the rate at which those lots are absorbed via housing starts.

- The New Home LSI came in at 81.6 for 4Q25, representing a 34.2% increase from 4Q24. For the first time since 2017, the 4Q25 data moved out of “significantly undersupplied” and into “slightly undersupplied” nationally.

- On a quarter-over-quarter basis, supply increased by 11.4% from 3Q25.

- The LSI counts the total vacant developed lot supply and adjusts it for overall starts activity.

“Policy uncertainty, the current cost of living, student loans, labor market concerns, interest rates, home prices, changes to immigration, geopolitics, and more have all slowed consumer demand,” said Ali Wolf, chief economist for Zonda and NewHomeSource. “When consumers aren’t happy, builders aren’t happy, and that’s exactly what we are seeing in the data. Builders have scaled back starts in response to slower sales, which by extension has allowed for lot supply to grow.”

Lot supply loosened year-over-year across nearly all major metropolitan areas, with New York and Minneapolis the lone exceptions

- Despite the loosening trend, lot inventory was still categorized as “significantly undersupplied” in 16 of 30 major markets in 4Q25.

- The markets where land supply loosened the most on a year-over-year basis were led by LA/OC, San Francisco, and Denver. Related, 4Q starts were down in LA/OC and Denver, while San Francisco starts were up 5%.

- Minneapolis tightened the most compared to the same time last year, falling 5.1% to 71.1, and was rated “significantly undersupplied.” Miami and San Diego were still the tightest lot markets in the country.

- Austin, Denver, and Dallas were the top 3 markets for loosest lot supply in 4Q, with Austin and Denver moving up to “significantly oversupplied” markets. The last time any top market was “significantly oversupplied” was Atlanta back in 2017. Dallas was rated as “slightly oversupplied,” along with Atlanta. Six other markets were “appropriately supplied,” with all other markets being “undersupplied.”

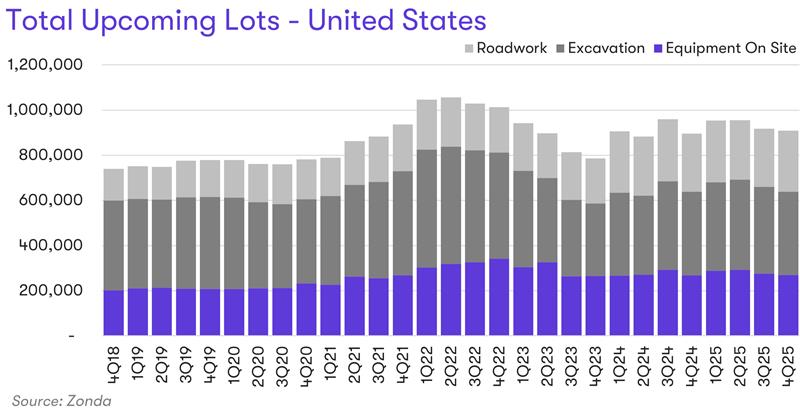

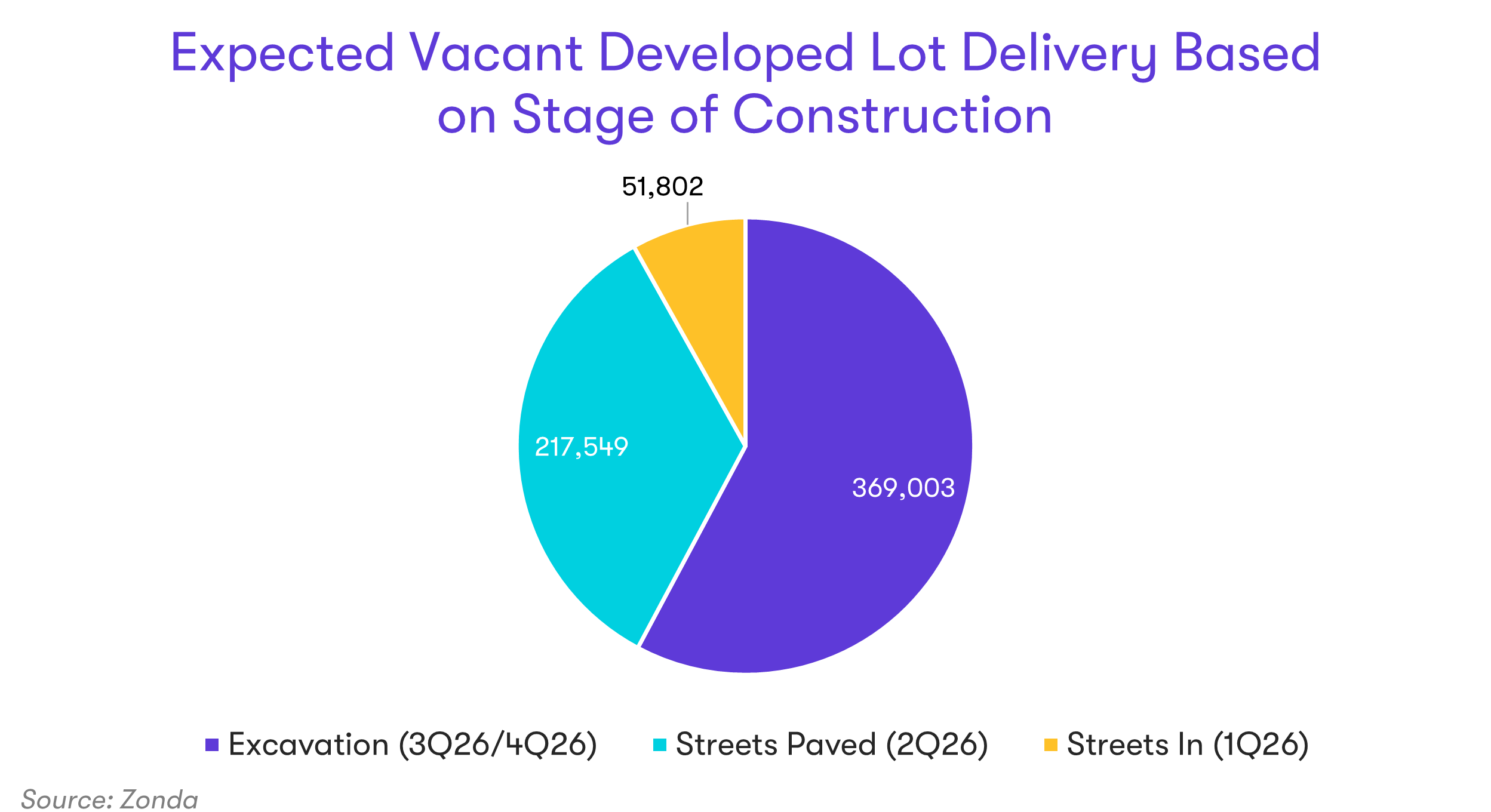

Zonda also records future lots through the stages of development. The stages range from raw land through streets in, which is the last step before the lot becomes a vacant developed lot. Zonda groups the last few stages into a classification called total upcoming lots, which typically indicates delivery over the next 12-18 months.

Total upcoming lots in 4Q25 increased 1.4% year-over-year but decreased 1.0% quarter-over-quarter. These types of lots were down 14.0% from the 2022 peak but were up 16.7% compared to the same quarter in 2019.

Among total upcoming lots, roadwork was up 4.8% year-over-year. Roadwork is comprised of the two smaller stages–streets paved and streets in–and represents the last step in lot development. Lots in the excavation stage were down 0.4% year-over-year, while those with equipment on site were up 0.7%.

The largest share of total upcoming lots were in the excavation stage in 4Q25, totaling 369K. These lots have an expected delivery between 3Q26 and 4Q26 (the range represents different timeframes from local entitlement processes). Note, not all of the lots in excavation will match Zonda’s estimated timeline.

“Seeing a reduction in the number of upcoming lots quarter-over-quarter is a positive sign considering current market conditions,” Wolf said. “While ongoing lot development remains important, it’s equally important to maintain discipline. If lot development drops too sharply, there could be a serious shortage when consumers eventually return to the market. On the other hand, moving forward too aggressively also poses risks, especially since there are already many vacant developed lots available today.”

Read past reports

Are you interested in reading past New Home Lot Supply Index reports? Access our report library to learn more.

Go deeper with Zonda Advisory services

Get more granular custom housing market data based on your region and your business needs. Learn more about our Advisory services to see how we can help you level up and meet your goals.

Methodology

The Zonda New Home Lot Supply Index (LSI) is built on proprietary, industry-leading data that covers the production new home market across the United States. The index values represent single-family vacant developed lot supply, lots that are ready to be built on, relative to equilibrium. Released quarterly, the New Home LSI provides an unrivaled look into the lot markets across the country, offering a current quarter snapshot as well as insight into the directional trend.

The New Home LSI is calculated based on each markets’ specific equilibrium as determined by our team of local experts and historical activity. The comparative current value is adjusted to capture the “true” months of supply figure by applying a greater weight to vacant developed lots in subdivisions with more starts activity. Each index value is associated with a phrase highlighting the current lot supply dynamics. A value of 100, represents perfect equilibrium, while a value of 125 and above equals “Significantly Oversupplied”, 115-125 – “Slightly Oversupplied”, 85-115 – “Appropriately Supply”, 75-85 – “Slightly Undersupplied”, and 75 and below – “Significantly Undersupplied.”

The foundation of the index is a quarterly release conducted by Zonda. It is necessary to monitor residential lot supply to understand how new home markets may be impacted by the incoming pipeline.